Contributing to IRAs is an excellent way to save for retirement. Traditional and Roth IRAs offer tax-advantaged benefits, either tax-deferred for a traditional IRA or tax-free for a Roth IRA. Which one is best for you, however, depends on your current and future financial circumstances. Even if your ability to predict the future is limited, you can follow a few IRA guidelines to get the biggest bang for your retirement dollars.

For 2024, the contribution limits for IRAs are $7,000 or the amount of earned income, whichever is less. An additional $1,000 catch-up contribution is available for those who are 50+. Contributions are allowed in both a Roth and a traditional IRA, but all IRA contributions cannot exceed $7,000 or $8.000 if 50+.

To contribute to a traditional or Roth IRA, you or a spouse must have earned income for the tax year. Earned income means from employment or self-employment. It does not include investment income, dividends, interest, or any other non-earned income.

Traditional IRA vs. Roth IRA

Whether you choose, or even qualify for, a traditional IRA, Roth IRA, or both, it’s vital to understand how they work. So, let’s start with a quick summary of each.

Traditional IRA features:

- Contributions are either pre-tax, after-tax or a combination of both.

- Earnings and growth are tax-deferred.

- After-tax contributions are not taxed when withdrawn, although you need to keep track of these contributions (Hint: set up a specific traditional IRA to hold only after-tax contributions).

- Withdrawals are taxed as income; a 10% penalty may apply if you withdraw money before age 59½.

- Required minimum distributions (RMDs) must begin at age 73.

- There is no age limit when you can make contributions, as long as you (or your spouse) have earned income.

Roth IRA Characteristics:

- Contributions are made on an after-tax basis. They are not tax-deductible.

- Earnings and growth are tax-free.

- Withdrawals are tax-free. Non-qualified withdrawals of growth or earnings may be subject to income taxes and a 10% early withdrawal penalty.

- Withdrawals of contributions are tax-free and penalty-free.

- There are no RMDs.

- No age limit for contributions as long as you or your spouse have earned income.

Sometimes, a deduction for a traditional IRA or contributions for a Roth IRA may be limited or even prohibited. The limits can get complicated, so we’ll break them down.

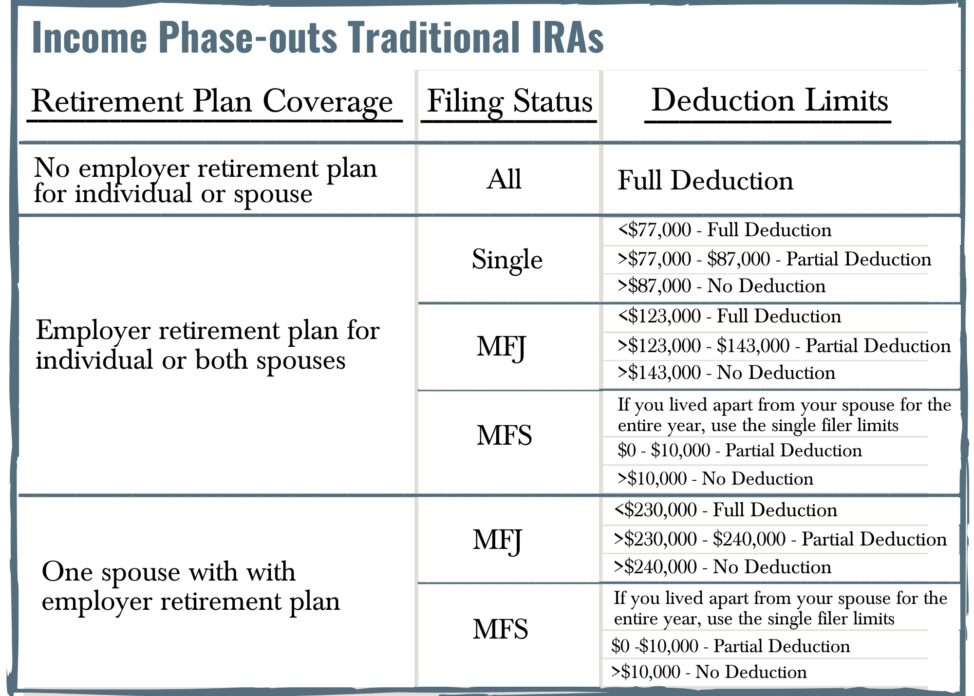

Traditional IRA Deduction Limits

Whether or not you or your spouse have a retirement plan, such as a 401(k), available through your employers determines the income limits for taking deductions for your traditional IRA. Please note this restriction limits your deduction but does not restrict your ability to contribute. The easy-to-read chart explains the different scenarios.

Again, these limits pertain only to the deductibility of an IRA contribution. Contributions are allowed, even if they are not deductible. For this reason, traditional IRA contributions must be designated as either deductible or nondeductible. When a tax deduction is taken, this amount, when withdrawn, is taxed. If nondeductible, no current deduction is allowed, but the amount is received tax-free when distributed. However, it may be subject to the aggregation rules.

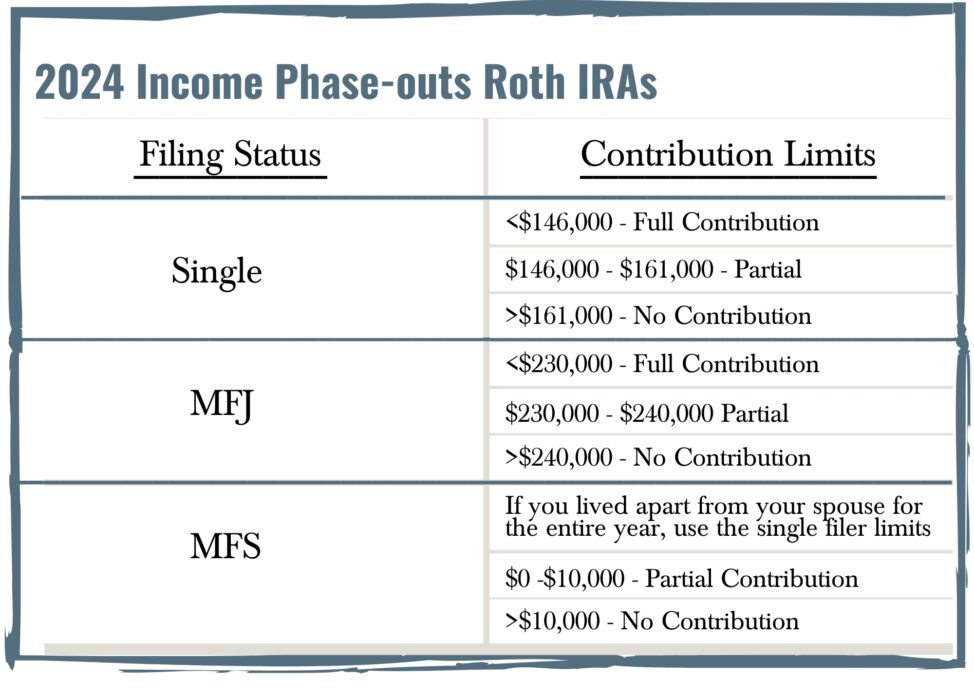

Roth IRA Contribution Limits

The Roth IRA income limits aren’t dependent on whether or not your employer has a retirement plan but are based on income.

Don’t qualify for a Roth IRA?

If you don’t qualify for a Roth but still want to set yourself up with some future tax-free retirement income, there is a way via the Backdoor Roth Strategy. Learn more in our blog post, How to Grow More Tax-Free Retirement Assets with Backdoor Roth Conversions.

Distributions

Although we’ve touched on some general distribution features of traditional and Roth IRAs, it’s time to dive into the distribution details.

Traditional IRA distribution rules:

- Qualified distributions from a traditional IRA are taxed as income.

- Distribution of after-tax contributions to a traditional IRA is tax-free.

- Money distributed before age 59½ is subject to a 10% penalty, with a few exceptions:

Distributions for Roth IRAs:

One of the most significant advantages of a Roth IRA is that contributions can be withdrawn at any time, tax-free and penalty-free. Earnings, on the other hand, can be withdrawn tax-free if the owner takes a qualified distribution.

Qualified distributions are tax and penalty-free:

- If you’re at least age 59½ OR satisfied the 5-year rule, whichever is later

- The 5-year rule requires that your first contribution to any Roth IRA must have occurred five years before the first distribution and assumes contributions were all made at the beginning of the year.

- If the distribution is due to your death or disability

- If the distribution is for a qualifying first-time home purchase (limit of $10,000) by you or a family member

Distributions of earnings that will incur taxes but avoid the penalty include:

- A 72t distribution, which is a series of substantially equal payments for five years or until age 59½, whichever is longer

- Unreimbursed medical expenses that exceed 10% of your adjusted gross income

- Distributions for the cost of medical insurance premiums if you’ve lost your job

- Higher education expenses for you or a family member

- IRS levy payments

- Qualified reservist distributions

- Qualified disaster recovery distributions

If these requirements are unmet and a withdrawal is taken, the earnings on invested Roth contributions are subject to income tax and possibly a 10 percent penalty. In this case, the withdrawal will be taxed on a first-in, first-out (FIFO) basis, which means that contributions will be considered the first withdrawn amount. Those amounts are subject to potential tax and penalty only when withdrawals exceed total contributions.

Roth vs. Traditional IRA: Which Type of IRA Is Best for You?

We’ve thoroughly reviewed the differences between traditional and Roth IRAs, but that only gets you so far. Understanding which is best for you requires more legwork and a crystal ball.

- Do you believe your tax bracket in retirement will be higher or lower than it is currently?

- Do you believe tax rates will increase or decrease in the future?

- Are you in your early, mid, or late career?

- What are your goals? Retirement income, estate planning, a little bit of both?

Do you believe you’ll be in a higher or lower tax bracket in retirement than you are now?

If you believe you’ll be in a lower tax bracket in retirement than you are now, it might be smart to use a traditional IRA. Contributing to a traditional IRA would result in avoiding a higher tax rate currently while paying taxes in retirement at a lower rate.

If, in your estimation, your tax bracket will be higher in retirement than it is now, you might lean toward a Roth IRA. Then, the tax you would pay on those contributions will be lower now than in retirement.

Do you believe tax rates will increase or decrease in the future?

The fact is that income tax rates are at historically low levels. The most recent tax law, TCJA, expires after 2025. So, what do you think will happen to future tax rates? Nope, it doesn’t take a rocket scientist to predict an increase in tax rates. Dollars taxed at a lower rate today, vs. probably higher future tax rates, do tip the scales towards Roth contributions.

What is your career stage?

If you’re starting your career, your income is probably much lower than it will be later. This higher income will bring a higher tax bracket and may even prevent you from contributing to a Roth IRA. That means it may be a good idea to contribute to a Roth IRA now at a lower rate.

What is your goal?

Another great feature of a Roth IRA, which often gets forgotten, is that it is an excellent estate planning tool. Roth IRAs are not subject to RMDs, so you can let those Roth dollars sit and grow until the cows come home. You can plan to pass a tax-free inheritance to your heirs.

Many clients have set up Roth IRAs with that exact intention. Of course, if you need tax-free funds for retirement, you’re free to take a distribution. You can take as much, as little, or nothing from a Roth IRA. It’s a quick and easy estate planning tool.

Not sure? Give yourself options

Why don’t you split the difference if you don’t know what the future holds (and who does?)? It’s smart to hedge your tax bets and contribute to both. If you do, it will give you options and limit your tax risks.

There is no one-size-fits-all when it comes to which IRA is best. Laws and situations change. What may be appropriate this year may not be next year. Although traditional and Roth IRAs are exceptional tools to save for retirement, it is vital that you continually analyze the most appropriate strategy and be ready to pivot to balance your current needs with your future needs.

I hope you found this post helpful. If you’d like to read more, please consider signing up for our monthly blog posts. You can do this via the sign-up form below.